Chancellor Rishi Sunak has written to accredited lenders about how the Government wants the Bounce Back Loan Scheme (BBLS) to be run. He has stated that as a 100% guaranteed loan scheme, the price of the BBLS is critical to its success and that lenders need to ensure that these loans are affordable and accessible.

With this in mind, he has come to the decision that the interest rate should be set at 2.5%.

Legislation and regulation

1. Amending the regulatory perimeter

The Treasury has made a statutory instrument (SI). This amends the Regulated Activities Order (RAO) so that providing regulated small business loans of £25,000 or less to sole traders, unincorporated associations and partnerships fewer than four people under the Consumer Credit Act 1974 (CCA), will not be a regulated activity for the purposes of BBLS.

This will enable small businesses to access their loans quickly. The SI retains the protections for these loans around debt collection, recognising that the importance of appropriate protections for borrowers who experience difficulties in paying back these loans.

2. Amending the CCA

The Government will introduce primary legislation at the earliest opportunity to disapply sections 140A-140C of the CCA for BBLS lending. The primary legislation will have retrospective effect, meaning that it will apply from the start of the scheme on Monday.

Interaction between BBLS and the Coronavirus Business Interruption Loan Scheme (CBILS)

Businesses will be able to borrow up to £50,000 under the BBLS, capped at 25% of turnover. In order to ensure that businesses have a clear understanding of the support available to them under the loan guarantee schemes, the minimum facility size for term loans and overdrafts under CBILS will increase to £50,001 to avoid any risk of confusion or overlap.

Any customer with a CBILS loan or overdraft of £50,000 or less will be able to switch that facility to a BBLS loan should they choose to do so over the next few months. This change to the minimum facility size will not apply to asset finance and invoice finance CBILS facilities.

Applying for the Business Bounce Back Loan (BBBL)

The government guarantees 100% of the loan and there won’t be any fees or interest to pay for the first 12 months.

Loan terms will be up to 6 years and no repayments will be due during the first 12 months.

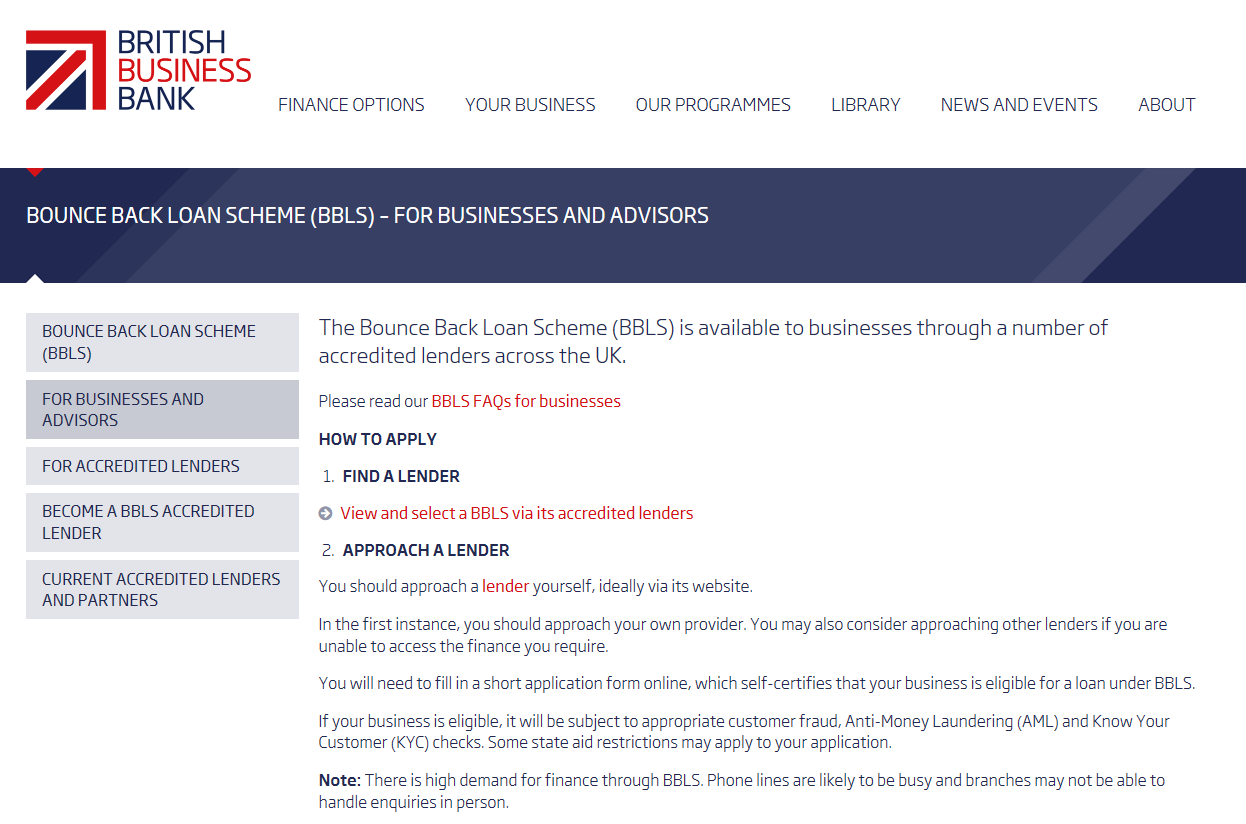

Full guidance on the application process can be found here but below we’ve detailed a brief outline.

Actions required:

- Find an accredited lender – there is a link to this on the above page.

- Approach them, ideally via their website.

- Complete a short application form which self-certifies that your business is eligible for a loan under BBLS.

- If eligible, you will need to complete the Banks Anti-Money laundering, fraud and Know Your Client checks.

- The lender makes a decision.

If you would like help applying for a BBBL, please don’t hesitate to get in touch and we’ll be more than happy to assist.

Who is eligible?

Your business must be able to self‑declare to the lender that it:

- Has been impacted by the coronavirus (COVID-19) pandemic.

- Was not a business in difficulty at 31 December 2019 (if it was, you must confirm your business complies with additional state aid restrictions under de minimis state aid rules).

- Is engaged in trading or commercial activity in the UK and was established by 1 March 2020.

- Is not using the Coronavirus Business Interruption Loan Scheme (CBILS), the Coronavirus Large Business Interruption Loan Scheme (CLBILS) or the Bank of England’s Covid Corporate Financing Facility Scheme (CCFF), unless the Bounce Back Loan will refinance the whole of the CBILS, CLBILS or CCFF facility.

- Is not in bankruptcy or liquidation or undergoing debt restructuring at the time it submits its application for finance.

- Derives more than 50% of its income from its trading activity (this requirement does not apply to charities or further-education colleges).

- Is not in a restricted sector (see below).

Note: The above is not an exhaustive list – see The British Business Bank for more information.

Bounce Back Loans are available to businesses in all sectors, except the following:

- Credit institutions (falling within the remit of the Bank Recovery and Resolution Directive).

- Insurance companies.

- Public-sector organisations.

- State-funded primary and secondary schools.

Frequently Asked Questions

The British Business Bank has released a list of FAQs for Small Businesses: Bounce Back Loan Scheme covering 24 questions.

If you have further questions about the scheme, please don’t hesitate to get in touch with PKB.

To read news and blogs from Rebecca Austin, click here >>